AI’s Efficiency Trap: When Productivity Destroys Demand

This is the second piece in a series. The first, Marx Was Right About AI, examined the leverage knowledge workers hold over AI deployment — and why mission-driven organizations will capture the productivity gains that extractive ones cannot. This piece operates at a different scale: not the firm, but the monetary system. Not the leverage window, but what comes after it closes. The third piece, The Robustness Imperative, asks what kind of AI infrastructure serves workers, organizations, and states — rather than extracting from them.

Every CFO in the world is running the same calculation right now. AI agents handle customer support at a fraction of the cost of a human team. AI tools compress the work of a ten-person analyst pool into two people and a model. Middle management layers — the coordinators, the report-generators, the meeting-schedulers, the escalation handlers, the performance reviewers, the translators of strategy into execution — can be partially or fully replaced by systems that don’t take vacation, don’t need health insurance, and don’t ask for raises.

The microeconomic logic is airtight. For any individual firm, deploying AI aggressively is not just rational — it is competitively mandatory. The firm that doesn’t move gets undercut by the firm that does. There is no opting out.

But the absence of choice at the firm level is important to state precisely. No CFO is deploying AI because they freely chose disruption. They are deploying it because the productive system — the accumulated fixed capital of the AI infrastructure now being built at scale — compels adoption through competitive pressure, exactly as the assembly line compelled adoption, exactly as offshoring compelled adoption. The technology does not spread because managers decide to adopt it. It spreads because the system leaves no firm the option of not adopting it. This is the installation period of a major technological revolution, operating according to its own logic, regardless of the human consequences it generates.

What no individual CFO’s spreadsheet captures is the fallacy of composition lurking inside every one of those efficiency calculations. What the productive system compels every firm to do individually becomes catastrophic in aggregate. And through the monetary framework developed by analyst Lyn Alden — in which economies are fundamentally flow systems, not stock systems — the aggregate picture is alarming in a way that quarterly earnings reports are structurally incapable of showing.

There is a second blindness in those spreadsheets, beyond the monetary one. The efficiency gains they record are not free. They are transferred — onto workers, onto energy grids, onto the climate, onto political systems — and transferred costs that don’t appear in a balance sheet do not thereby cease to exist. This is the same structural blindness that made offshoring look like pure gain, that made fossil fuels look cheap for a century, and that is now making AI look like frictionless productivity. The externalities are real. They are simply someone else’s problem, for now.

This piece traces both blindnesses — the monetary and the ecological — to their convergence point. That convergence is not comfortable. But it opens a question that purely financial analysis cannot ask: what if the disruption is not just a crisis to be managed, but a forced transition that could, under the right political conditions, be the beginning of something necessary?

I. Lyn Alden’s Spending Loop#

Alden’s core insight, developed across her research and in Broken Money (2023), is deceptively simple: money only has value when it moves. An economy is not a warehouse of accumulated wealth. It is a circulatory system. The health of the system depends not on how much money exists but on how fast and how broadly it flows.

The primary pipe in that circulatory system is wages. Workers receive wages. They spend those wages on goods and services. That spending becomes revenue for other firms. Those firms pay wages to their workers. The loop closes and repeats. Break the pipe anywhere in sufficient volume, and the loop doesn’t just shrink — it can spiral downward, each contraction triggering the next.

Alden draws a distinction that is critical for understanding what AI does to this system. Profit income and wage income do not behave the same way monetarily. Wage earners — especially middle-income wage earners — spend the vast majority of what they receive, almost immediately, back into the economy. It pays rent, groceries, car payments, children’s activities, the occasional restaurant meal. The velocity of wage income is high. It circulates.

Profit income — the income that accrues to shareholders and senior executives when AI replaces a human — behaves very differently. It tends to save, to invest in financial assets, to fund stock buybacks, to sit in brokerage accounts. Its velocity is low. It pools rather than flows.

This is not a moral argument. It is a mechanical one. When AI transfers income from the wage category to the profit category at scale, it does not leave the monetary system neutral. It slows the circulatory system — quietly, diffusely, and with a lag long enough that no single earnings report will flag it as a cause.

This transfer is not the result of decisions that could be made differently within the existing system. It is the structural function of fixed capital investment. Capital invests in AI to increase the rate of surplus extraction from labor. The surplus flows to the capital layer. The wage pipe narrows. This is not a side effect — it is the point. Carlota Perez, in Technological Revolutions and Financial Capital (2002), describes this as the characteristic monetary signature of every installation period: financial capital captures the gains while the institutional framework that would distribute them has not yet been built, and will not be built without a political fight.

We have a preview of the monetary consequences. After 2008, central banks flooded the financial system with liquidity through quantitative easing. Capital was abundant. But without wage growth, consumption remained structurally weak for a decade. Asset prices inflated. Main Street stagnated. The Fed was pushing on a string because the problem was never liquidity — it was the broken wage pipe. AI, deployed at scale by the compulsion of the productive system, is the same mechanism, running faster and with greater reach.

II. The First Loop: Who Actually Gets Displaced#

The standard reassurance about AI displacement follows a familiar script: yes, some jobs will be lost, but new jobs will emerge, as they always have. The Industrial Revolution displaced agricultural workers; they became factory workers. Factory automation displaced assembly line workers; they became service workers and managers. The pattern holds, the argument goes. Trust the pattern.

The argument fails for two reasons, one about who and one about speed.

On who: previous automation waves primarily displaced manual and routine cognitive labor. The displaced could move up the value chain — into supervisory roles, into coordination, into the administrative and managerial infrastructure that growing organizations needed. That infrastructure absorbed them. It was the reabsorption layer — the category that grew as the one below it was automated.

The fixed capital system has now automated the reabsorption layer itself.

Middle managers are the most structurally exposed category in the global workforce, and almost entirely absent from public discussions about AI displacement, which tend to focus on call center workers or truck drivers. This is a significant analytical error. The middle manager’s core functions — synthesizing information from below, translating strategy from above, allocating resources, monitoring performance, generating reports, handling escalations, running the coordination layer of organizations — are precisely and specifically what AI agents are being built to do. The general intellect, embodied in fixed capital, is automating the humans whose function was to coordinate the deployment of previous fixed capital.

This is not a niche observation. It applies to every industry, in every geography, at every organizational scale. The regional manager of a retail chain. The claims supervisor at an insurer. The project manager at a construction firm. The department head at a hospital administration. The operations coordinator at a logistics company. The account manager at a bank. The team lead at a software company. Every one of these roles is fundamentally a coordination, synthesis, and reporting function. Every one of them is in the direct path of agentic AI deployment.

This is global. It is not a Silicon Valley story or an Anglo-American story. Every multinational, every regional bank, every government ministry, every hospital network on every continent runs this management infrastructure. The displacement will be uneven in timing — richer, more digitized economies first — but the structural exposure is universal.

Below middle management, the displacement is equally broad. The analysts who feed information upward. The executive assistants who manage schedules and communications. The junior lawyers who conduct research and draft initial documents. The junior consultants who build the slide decks. The customer success managers who handle routine client issues. The financial analysts who produce the monthly reports. These are the $60,000–$150,000 earners in developed economies — and their equivalents globally — who are mortgage holders, car buyers, whose spending constitutes the discretionary consumption that retail, hospitality, media, and services depend on.

They are not the precariat. They are the engine of middle-class consumption. And they are the primary target of the current wave of fixed capital deployment.

On speed: past automation waves moved at the pace of physical capital deployment. A factory had to be built. Machines had to be installed. Workers had to be retrained on specific equipment. The transition took decades. New job categories had time to emerge organically. Labor markets had time to adjust.

AI is software. It scales instantly across millions of deployments simultaneously. It crosses sectors at once rather than one industry at a time. A model that can handle insurance claims can handle legal research can handle financial analysis can handle project coordination — not sequentially, over decades, but concurrently, within years. The productive system is not constrained by the speed of physical installation. The compulsion propagates at the speed of software adoption.

Speed is everything for the reabsorption argument. New job categories only help if they emerge before the displaced exhaust their savings and reduce their consumption. The window is narrowing faster than any historical precedent suggests is manageable.

III. The SaaS Aipocalypse: The Second Loop#

There is a second destruction loop running in parallel that receives almost no attention in mainstream economic commentary, because it requires understanding the structure of the software industry to see it.

The last two decades produced an enormous layer of B2B software — SaaS companies selling workflow tools to businesses. CRM platforms. Customer support platforms. HR management tools. Financial planning software. Project management tools. Marketing automation. Legal research platforms. Each of these businesses built their revenue model on seat-count economics: more humans using the software means more licenses, more seats, more revenue. The model assumed the humans doing the work would always need software to do it.

AI agents do not need seats. They complete the workflow without the human operator in the loop. And they are being deployed now, at scale, by the same businesses that were paying for those seats.

Chegg is the starkest public example. The educational services company watched its stock fall over 95% from its peak. Its CEO named ChatGPT directly as the cause. Students who would have paid for Chegg subscriptions were getting their answers from a free AI. The seat-count model evaporated almost overnight.

Chegg is not an isolated case. It is a preview. Zendesk, Intercom, Freshdesk — the customer support SaaS stack — are watching AI agents handle the tier-1 and tier-2 support interactions that justified their per-seat pricing. Intercom’s own product, Fin, is an AI agent that does exactly this. They are cannibalizing their own revenue model in order to survive — the only available move in a market where competitors will do it to you if you don’t do it first. Salesforce is in the same position with Agentforce. Every AI-powered CRM agent they sell reduces the number of human operators their customers need, reducing the seat count that Salesforce’s own revenue depends on.

This is the productive system’s compulsion made visible at industry scale. No SaaS company can choose not to add AI. Every SaaS company that adds AI accelerates the destruction of the seat-count model the entire industry was built on. The fixed capital logic offers no exit. Each firm does the individually rational thing. The industry destroys its own revenue model in aggregate.

The monetary consequences compound the first loop. SaaS companies lose revenue. They cut headcount — highly paid engineers, salespeople, customer success managers, product managers in expensive cities with high consumption footprints. Those workers reduce spending. They were themselves consumers of cloud services, developer tools, and other SaaS products. The second loop feeds back into the first.

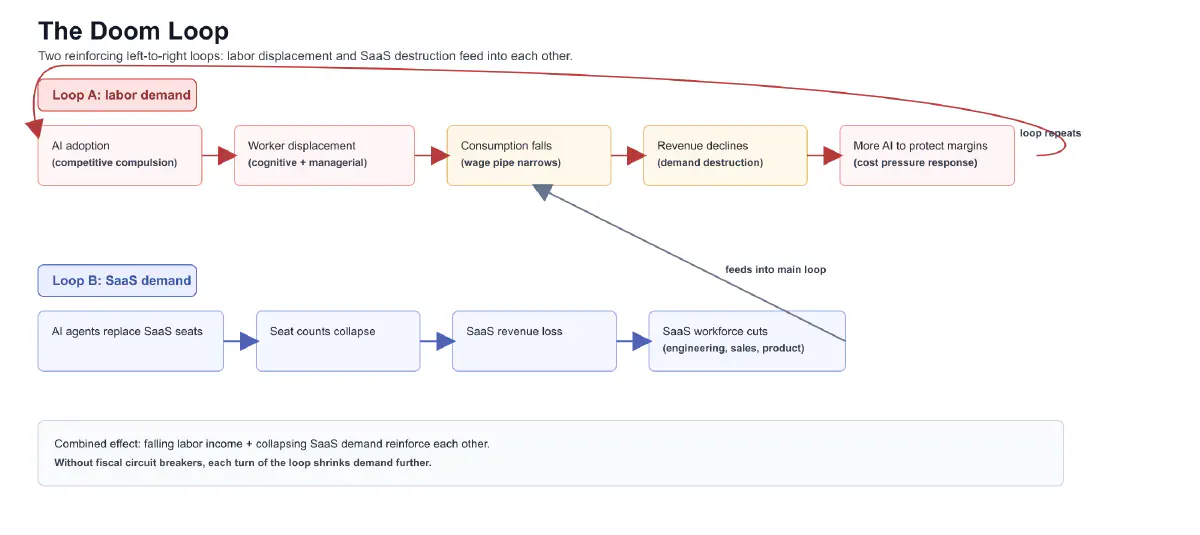

IV. The Doom Loop#

Put the two loops together and run them through Alden’s flow framework. The result is not a policy failure or a management error. It is the automatic output of the productive system operating according to its own logic:

Companies adopt AI — not by choice but by competitive compulsion. Workers are displaced across every sector, at every level, concentrated in the middle-income cognitive and managerial work that drives discretionary consumption. Those workers reduce spending. Consumption falls. Corporate revenues — which depend on consumption — eventually follow. Companies respond by deploying more AI to protect margins. More workers are displaced. The loop runs itself.

Simultaneously: the productive system compels AI agent adoption. SaaS seat counts collapse. SaaS companies lose revenue and cut their own highly-paid workforces. Those workers reduce spending. The second loop feeds into the first and tightens further.

The asset price signal will be misleading throughout this process, possibly for years. AI adoption genuinely improves corporate margins in the short term. Earnings beat expectations. Analysts upgrade targets. Equity markets rise. The efficiency gains are real — they accrue to the profit layer rather than the wage layer, which means they inflate asset prices rather than consumption.

The demand destruction shows up elsewhere first, in forms easy to misread as cyclical rather than structural. Credit card delinquency rates, already at post-2008 highs in 2024, continue rising. Personal savings rates, already near historic lows, fall further as households try to maintain consumption on reduced income. Retail closures accelerate. Commercial real estate deteriorates further. Regional banks with concentrated exposure show stress.

None of this will be attributed to AI displacement in the quarterly commentary. It will be called a soft landing, a consumer slowdown, a credit normalization. By the time the connection is legible in the data, the loop will be self-reinforcing.

This is the structure Alden’s framework makes visible that standard GDP accounting obscures. GDP measures output. It does not measure the distribution of claims on that output, or the velocity at which those claims circulate. An economy can post positive GDP growth while the monetary loop quietly strangles — if the growth is concentrated in the asset-price layer while the wage pipe narrows. We have been living this dynamic in partial form since 2008. The productive system’s AI deployment is the accelerant.

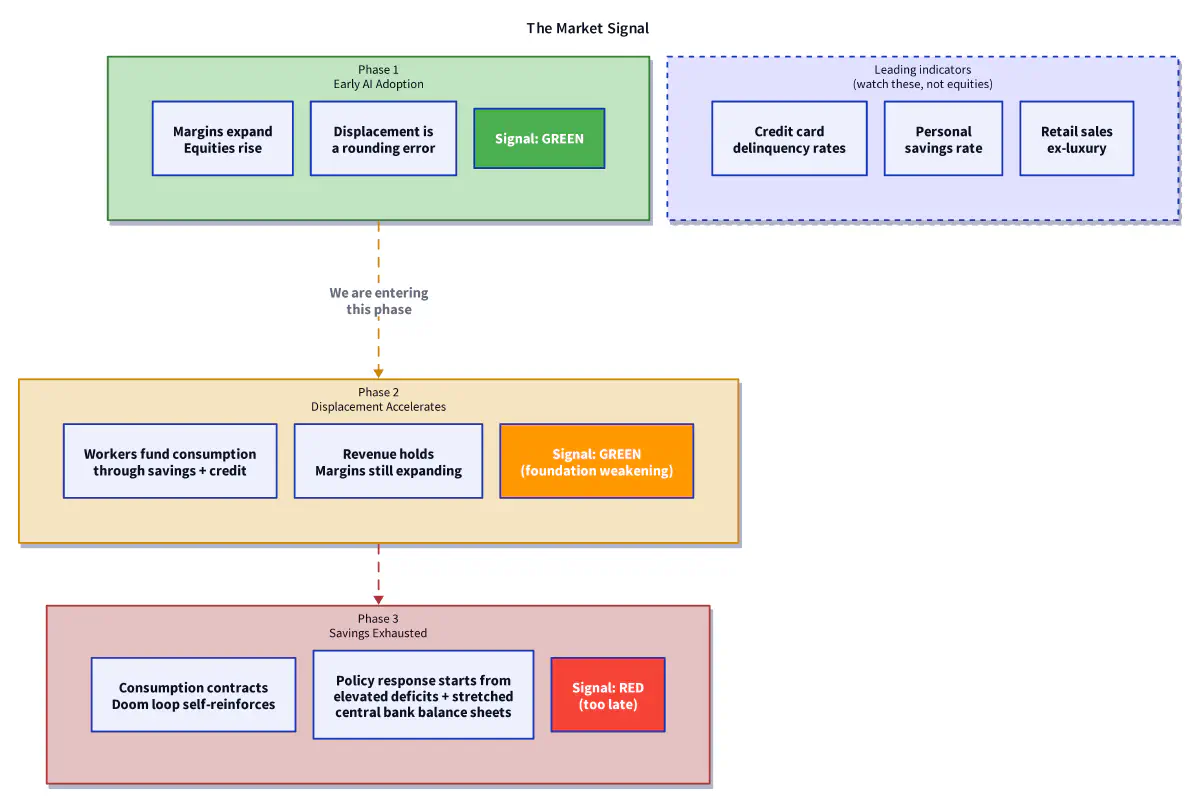

V. The Asset Price Illusion and Why Markets Won’t Warn You#

It is worth dwelling on why the standard market signal will fail here, because this is where most financially literate readers will push back. If AI displacement were genuinely threatening aggregate demand, surely bond markets would price in deflation risk. Surely credit spreads would widen. Surely equity markets would price in the revenue risk from falling consumption.

They will — eventually. But the sequencing creates a dangerous lag that mirrors Perez’s installation period exactly: financial capital benefits from the early phase, and the market signal reflects financial capital’s experience, not the wage layer’s.

In the first phase, AI adoption is unambiguously positive for corporate earnings. Margins expand. Revenue grows, because the companies deploying AI are still selling into a consumer base not yet meaningfully displaced. The workers being laid off in early AI waves are a small fraction of total employment. Their reduced consumption is a rounding error. Equities rise. Spreads remain tight. The signal is green. This is the installation period at its most seductive.

In the second phase, displacement accelerates. But the affected workers initially manage their spending through savings drawdowns and credit. The consumption signal remains stable, funded by debt. Corporate revenues hold. Margins continue expanding. The signal is still green, but the foundation is weakening invisibly. This is the phase we are entering.

In the third phase, savings are exhausted, credit is maxed, and consumption contracts in earnest. This is when the revenue signal finally turns. But by this point the displacement is deep, the doom loop is self-reinforcing, and the policy response is starting from already-elevated government deficits and already-stretched central bank balance sheets. This is Perez’s crisis — the hinge between installation and deployment — and it is the moment when the question of who benefits from the deployment period becomes a political emergency rather than an academic argument.

The warning will come from consumer credit data, not from equity markets. Watch delinquency rates. Watch the personal savings rate. Watch retail sales ex-luxury. These are the leading indicators of the broken wage pipe — and they are already pointing in the wrong direction before the main wave of AI displacement has landed.

VI. Circuit Breakers — And Why They Are Politically Blocked#

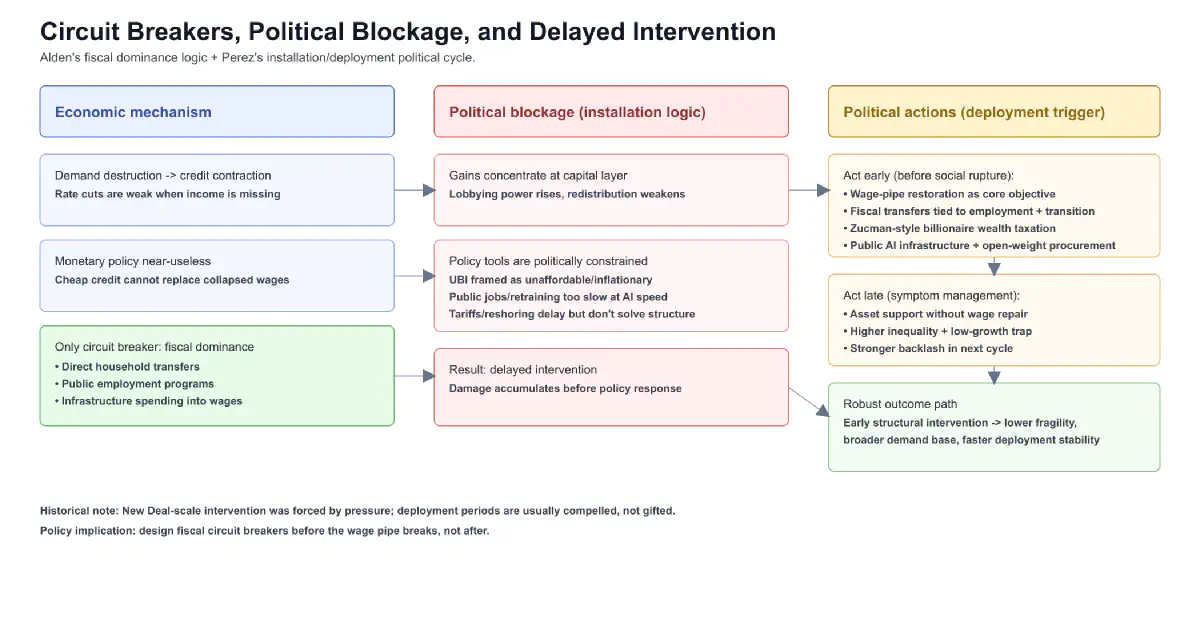

Alden is explicit: in a credit contraction driven by demand destruction, monetary policy is nearly useless. Cutting interest rates does not help when the problem is not the cost of credit but the absence of income to service it. The Federal Reserve lowering rates to zero while middle-class consumption collapses is the same movie as 2008–2015, at higher speed and larger scale.

The only mechanism that creates net new money into the private sector — Alden’s term is fiscal dominance — is government spending. Direct transfers to households. Public employment programs. Infrastructure investment that puts wages into the economy. And financing architecture matters: progressive taxation of concentrated wealth — including Zucman-style billionaire wealth tax proposals within broader wealth tax frameworks — is one way to fund the circuit breaker while reducing concentration pressure. This is the circuit breaker. It is the only circuit breaker. And it is politically radioactive in every major economy simultaneously.

This blockage is not accidental. The productive system’s installation period generates the political conditions for its own perpetuation: the concentration of gains at the capital layer funds the lobbying and political influence that resists redistribution. The same dynamic played out in every previous technological revolution. The New Deal did not happen because capital decided to be generous. It happened because the political pressure of mass unemployment became impossible to manage without structural intervention. The deployment period of the mass production revolution was forced, not offered.

Universal Basic Income — the most direct monetary intervention — is dismissed in mainstream policy circles as unaffordable, inflationary, or philosophically objectionable. Public employment programs are slow and bureaucratically constrained. Retraining programs have a poor track record at the scale required and assume the jobs being trained for will still exist by the time training is complete. Tariffs and reshoring mandates delay the problem without addressing its structure.

What Alden’s framework predicts — and what Perez’s historical analysis confirms — is that governments will eventually intervene massively when the political pressure becomes impossible to ignore. The question is not whether. It is how much damage accumulates before the intervention arrives, and whether it is designed to address the structural problem or only to manage the immediate political symptoms.

The post-2008 response is the cautionary case: it primarily inflated asset prices without repairing the wage pipe, produced a decade of low growth and rising inequality, and created the political conditions for the current moment. An equivalent response to AI-driven demand destruction — quantitative easing while the wage pipe collapses — would be the same error at larger scale.

VII. The Externality Trap: What the Spreadsheet Doesn’t Count#

There is a word for costs that are real but don’t appear in a balance sheet: externalities. And the history of neoliberal economic management is, in large part, a history of mistaking the absence of externalities from accounting for their absence from reality.

The CFO spreadsheet that books an AI efficiency gain belongs to a long lineage of incomplete accounting. The spreadsheet that made offshoring look like pure gain ignored the social costs of deindustrialization transferred onto communities, healthcare systems, and political stability. The spreadsheet that made fossil fuel energy look cheap for a century ignored the carbon costs transferred onto the atmosphere. In both cases, the externalities were real, they were deferred, they were diffused across the commons — and they eventually returned as someone else’s crisis, at a scale that dwarfed the original gain.

The AI efficiency calculation is the same structure, running at greater speed and across more domains simultaneously.

AI’s externalities are specific and measurable, even if they are not being measured:

Energy and water consumption. The compute infrastructure required to run frontier AI models is staggeringly material. Microsoft, Google, and Amazon are building or contracting nuclear plants specifically for AI workloads. Data center electricity consumption is projected to double or triple by 2030. Cooling these facilities requires water at significant scale — in regions already under water stress. Training a single large language model produces carbon emissions comparable to multiple transatlantic flights. None of this appears in the efficiency calculation of the firm deploying the model. It is transferred onto grids, water tables, the atmosphere, and eventually everyone’s electricity bill.

Geographic concentration of infrastructure. The compute layer is controlled by five companies in two countries. The efficiency gains are extracted globally — from workers in every country, from SaaS markets in every economy — but the infrastructure and its returns are captured in a handful of data centers and balance sheets. The gains are privatized globally. The infrastructure costs are borne locally.

Labor displacement costs. Transferred onto unemployment systems, retraining programs, healthcare systems, and the political stability that functioning economies depend on. These are fiscal costs — they will appear eventually, in government expenditure — but they are invisible to the firm that captured the efficiency gain. The firm books the profit. The state absorbs the consequence.

This is what Herman Daly identified in Beyond Growth (1996) as the fundamental flaw of GDP accounting: it measures throughput but not the depletion of the natural and social capital that makes throughput possible. A forest that is clear-cut contributes positively to GDP. The loss of its carbon sequestration, watershed protection, and biodiversity does not subtract. The accounting is not neutral. It is systematically biased toward extraction and against the preservation of the systems that make extraction possible.

Lyn Alden and Herman Daly are making the same observation at different scales. Alden: the monetary accounting is incomplete because it measures flows to capital but ignores the destruction of wage-pipe velocity. Daly: the economic accounting is incomplete because it measures throughput but ignores the depletion of natural capital. AI makes both gaps visible simultaneously, in the same transactions.

The CFO spreadsheet that books an AI efficiency gain is simultaneously:

- Reducing wage-pipe velocity — Alden’s missing variable

- Externalizing energy and carbon costs onto the commons — Daly’s missing variable

- Booking both omissions as profit

This is not an argument that AI should not be deployed. It is an argument that the accounting is incomplete, the gains are being privatized, and the costs are being socialized — and that the reckoning for that mismatch is not optional. It is only a matter of when and how, and who is in the room when the bill arrives.

VIII. The Planetary Question — Catastrophe or Forced Transition?#

Here the analysis has to confront an uncomfortable possibility that most macroeconomic commentary refuses to take seriously.

The framework so far assumes that the goal is to restore the growth loop — repair the wage pipe, reinject demand, return the economy to compound annual growth. Alden’s circuit breakers operate within this assumption. But what if the loop should not resume at its previous rate?

The Limits to Growth — the 1972 Meadows et al. report that modeled the interaction between exponential growth and finite planetary systems — predicted this collision with uncomfortable precision. The standard run scenario, which assumed no major changes to historical growth patterns, projected resource overshoot and economic decline in the early twenty-first century. Subsequent analysis tracking the report’s predictions against actual data has found the standard run scenario performing disturbingly well. We have already exceeded six of nine planetary boundaries. A 3% annual growth rate doubles the global economy every 24 years. The physical substrate for permanent compound growth does not exist.

The standard capitalist response is the decoupling thesis: AI will allow us to produce more value with fewer material inputs, permanently separating growth from throughput. The general intellect, embodied in models rather than steel and oil, is the first fixed capital system that appears to have no physical frontier.

This is where the previous section bites back. The physical footprint of AI is not minimal. It is enormous and growing. The decoupling thesis for AI is false at the infrastructure level — the data centers, cooling systems, GPU supply chains, and energy contracts are deeply material. And the empirical record of absolute decoupling more broadly, despite decades of promises, remains thin. Relative decoupling — fewer resources per unit of GDP — is real but has never been fast enough to offset the scale of growth. Jason Hickel’s argument in Less Is More (2020) holds: degrowth is not a policy preference. It is a physical reckoning that will happen by design or by collision.

So here is the question the efficiency trap forces into view: if AI-driven displacement produces a structural reduction in aggregate demand, and if that manifests as prolonged below-trend economic growth — is that catastrophic, or is it the forced degrowth transition the planet requires?

The answer is: it could be either. Which one it becomes depends on political choices that are not currently being made — specifically, on who controls the redistribution mechanism and whether the state uses fiscal dominance to route the productivity surplus back into the wage pipe or allows it to pool in the asset layer.

AI-driven degrowth without redistribution is straightforwardly catastrophic. Displaced workers do not consume less cleanly. They consume more desperately and cheaply — lower-quality food, deferred healthcare, cheaper and dirtier energy, reduced investment in their children’s futures. The ecological footprint of poverty is not low. It is differently destructive. An economy contracting at the wage-layer bottom while the asset layer expands is not a degrowth transition. It is immiseration with a stock market rally.

AI-driven degrowth with redistribution — a managed transition in which the productivity surplus is genuinely shared, displaced workers have sufficient income to participate in a lower-throughput economy, and fiscal policy is designed around sufficiency rather than growth restoration — could be something different. It could be the mechanism by which high-income economies begin to live within planetary limits. Not as a moral project. As an economic and political inevitability, arrived at through the back door of the fixed capital system’s own logic.

The Jevons Paradox introduces a critical complication here. William Stanley Jevons observed in 1865 that making coal engines more efficient increased total coal consumption — lower cost expanded use cases faster than efficiency reduced consumption per case. The same dynamic applies to AI. As models become cheaper and more capable, deployment accelerates. Cheaper AI is not less disruptive AI. It is more disruptive AI, deployed more broadly, by the same compulsive logic of the productive system.

But the Jevons effect cuts in a second direction that is less discussed. When capable models run locally at near-zero marginal cost — a credible ten-year trajectory — the question of who has access to AI changes fundamentally. Today, AI deployment at scale requires hyperscaler infrastructure and technical expertise concentrated in wealthy firms in wealthy countries. In ten years, a smallholder cooperative in Kenya, a public health clinic in rural India, a municipal government in a mid-sized Latin American city could run capable AI locally, for free. The value created stays local. The wage pipe gets rebuilt from below rather than drained from above. The open model ecosystem — Llama, Mistral, DeepSeek — is the early technical signal that this trajectory is viable.

The condition is not technical. It is political. This only happens if the infrastructure layer — open weights models, local compute, energy access — is treated as a public good rather than a proprietary advantage. Without that choice, the Jevons acceleration is just faster displacement, more diffuse damage, and a global demand void arriving sooner than anyone is pricing. With it, the deployment period Perez describes could be genuinely different from the post-war settlement — not built on resource extraction and geographic expansion, but on distributed cognitive infrastructure that keeps the productivity surplus local.

IX. What a Managed Transition Requires#

Putting the monetary and planetary arguments together, the policy prescription becomes more specific than “spend more.”

The circuit breakers for the monetary crisis — UBI, public employment, direct fiscal transfers — are also, if designed correctly, the mechanism for a managed degrowth transition. A household with a guaranteed income floor consumes differently than a household in precarity. It consumes less compulsively, less cheaply, less environmentally destructively. It has the security to participate in a lower-throughput economy without the panic consumption that poverty produces.

This is the convergence point between Alden’s monetary framework and Raworth’s doughnut model. Alden says: maintain the spending flow or the monetary system contracts. Raworth says: the spending flow must be redesigned to stay within planetary boundaries. A redistributive fiscal response to AI displacement — one that maintains consumption capacity without restoring growth-at-all-costs — threads both needles simultaneously.

The “who benefits” question is the fulcrum. Every previous technological revolution produced a deployment period eventually — the railways, electrification, mass production all eventually distributed their benefits more broadly than the installation period suggested they would. But this did not happen automatically. It happened because workers organized, because political systems faced irresistible pressure, because the alternative — permanent mass unemployment and demand collapse — was politically unsustainable. The post-war settlement was not a gift from capital. It was the price of social stability.

The AI deployment period will be determined the same way. Not by the logic of the productive system, which will continue to concentrate gains at the capital layer until forced to do otherwise. Not by the good intentions of technology companies, which are structurally unable to prioritize wage-pipe maintenance over shareholder returns. But by the political pressure of people who understand the mechanism and are willing to name it as what it is: not a natural disaster, not an inevitable consequence of progress, but the output of a productive system operating according to its own logic — a logic that can be redirected, if the political will exists to do so.

The distance between what is being done and what needs to be done is itself important information. Naming it clearly is the first act of the managed transition.

Coda: The AGI Horizon#

Everything above assumes that human cognitive labor remains economically relevant. It is worth naming, plainly, that this assumption has a finite shelf life.

The trajectory of AI capability over the next decade is uncertain in its details but not in its direction. Models are becoming more capable, cheaper to run, and more broadly deployable on a curve that has not shown signs of flattening. The ten-year horizon on which capable models run locally at near-zero cost is also the horizon on which artificial general intelligence — systems that can perform any cognitive task a human can perform — moves from speculative to plausible.

If AGI arrives within that window, the analysis above describes the transition period accurately but not the destination. Alden’s framework assumes wages are the primary mechanism for distributing productive capacity to households. If cognitive labor becomes effectively free and unlimited, that assumption breaks at the foundation. This is not a monetary crisis. It is a question about what money, work, and economic participation mean in a post-labor economy. No existing framework answers it adequately, because no existing framework was built for it.

The degrowth framing partially survives — planetary limits are real regardless of who or what is doing the producing — but degrowth economics was built around human economic activity as the unit of analysis. AGI scrambles that unit in ways the field has not yet seriously engaged with.

What can be said is this: the managed transition described in this piece — redistribution, open infrastructure, fiscal policy for sufficiency — is the prerequisite for navigating the AGI horizon humanely. Societies that have built robust income floors, genuinely public AI infrastructure, and political systems capable of managing technological transition deliberately will be better positioned for whatever the AGI horizon produces than societies that arrived there through unmanaged crisis.

The efficiency trap is not a problem AI creates. It is a problem that pre-existing political choices — to privatize gains, to externalize costs, to treat the monetary system as self-correcting and the planet as an infinite sink — have made AI into. The technology is not the cause. It is the accelerant. The fire was already burning.

Whether what comes next is catastrophe or transition depends on choices being made right now, mostly by people who are not framing them as choices at all.

Further Reading#

- Lyn Alden, Broken Money (2023) — the monetary framework underlying this analysis; essential on why fiscal and monetary policy are not the same thing

- Lyn Alden, Fiscal Dominance and the Return of Zero-Interest Bank Financing — what happens when monetary policy loses traction in a demand contraction

- Carlota Perez, Technological Revolutions and Financial Capital (2002) — the installation and deployment period framework; why the current extraction is the historical pattern, and what determines who benefits from the deployment period

- Donella Meadows et al., The Limits to Growth (1972) — the foundational systems model of planetary limits; the standard run scenario has tracked actual data with uncomfortable accuracy for fifty years

- Herman Daly, Beyond Growth (1996) — the economic argument that GDP accounting is structurally blind to natural capital depletion; the Alden of ecological economics

- Kate Raworth, Doughnut Economics (2017) — planetary boundaries meet economic model; the framework for sufficiency over perpetual growth

- Jason Hickel, Less Is More (2020) — the most direct contemporary argument for degrowth as civilizational necessity

- William Stanley Jevons, Jevons Paradox (The Coal Question, 1865) — the original statement of the rebound effect; reads as contemporary

- Daron Acemoglu & Simon Johnson, Power and Progress (2023) — who historically captures gains from transformative technology, and why workers benefiting is never the automatic outcome

- Harry Braverman, Labor and Monopoly Capital (1974) — how capital systematically deskills labor; the baseline the current moment is breaking from

- Karl Marx, Fragment on Machines (Grundrisse, 1858) — the general intellect argument, written 170 years before it became literally true

Comments (Mastodon)

Comment on Mastodon